You’ve heard the statistic that half of all new businesses fail within the first five years, right? While I haven’t seen the same statistic about nonprofits, I’d venture a guess that it’s a similar number. In fact, the Nonprofit Times released a study in early 2018 that claimed “most charities are teetering on financial peril”.

Financial peril. Intense words to sit with.

So let’s think about that. Fifty percent of organizations, created to do more good in the world and serve those in need, are disappearing, dissolving, or closing up shop on a regular basis which means that whatever need they were created to fill is still out there. That means 8% of organizations are currently operating in the red and 30% are on the verge. We’re talking about spending more than you’re bringing in and not having enough cash to pay your bills.

The question is WHY? Perhaps there wasn’t a strong enough need for the product or service, leadership was not aligned on long-term planning, they weren’t able to bring in enough revenue to cover expenses, there were too many other organizations or companies doing the same thing, or they weren’t providing enough value to the people they were serving.

The bigger question is HOW do we avoid financial peril and ultimately failure? How do we ensure that nonprofit organizations, created to drive positive change in the world, are financially sustainable so they can continue helping and serving, year after year?

I’ve found a solution and I am thrilled to share it with you because it’s an industry game-changer.

But first, even if your organization manages to pay its bills and make payroll every month, do you have a long-term cash management plan? Do you have a reserve of 3-6 months of operating expenses? Do you lose sleep at night (or at least worry occasionally) that your nonprofit seems like a cash-sucking monster and your fundraising just can’t keep up?

I thought so. Keep reading.

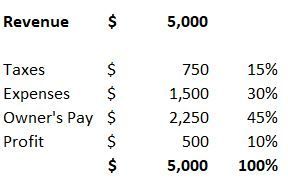

As an entrepreneur who’s always interested in improving myself and my business, I recently devoured Profit First, a book by Mike Michalowicz. He has worked with hundreds of business owners who are slaves to their businesses, miserable, and not making any money. His solution to the problem of business owners not making any money is reframing the traditional thinking of Revenue – Expenses = Profit. Instead of taking whatever is left over as profit, he encourages business owners to take their profit first, so Revenue – Profit = Expenses. In other words, bring in the money, set aside a percentage for profit, and use the remainder for expenses.

You’ve probably heard of Parkinson’s Law: work expands so as to fill the time available for its completion. In other words, if you have 8 hours to complete a task, it will take you 8 hours. If you have 2 hours to complete the same task, it will take you 2 hours. The productivity gurus out there LOVE this (give yourselves deadlines, people!).

Well, Michalowicz says the same thing about money. If you have $20,000 to spend on operating expenses, you will spend $20,000. If you have $50,000, you will absolutely spend $50,000. This becomes a major problem when you don’t take your profit first, because you will have spent that $50,000 before you can set aside your profit, and before you know it, you have nothing left over.

Michalowicz then goes into exactly HOW to take your profit first and it involves setting up a bunch of bank accounts, reviewing your numbers twice a month, and separating your cash according to a handful of formulas he provides. According to his case studies, this method WORKS.

Now that you have the major premise of the book, it really makes logical sense, right?

But what about nonprofits? Nonprofits don’t make a profit. The Executive Director isn’t personally pocketing a portion of grants each month (at least I REALLY hope not!). And what about restricted funding? You can’t just hack off a portion of a grant and set it aside, right?

You’re right that nonprofits aren’t looking to make a profit, but what they ARE looking for is FINANCIAL SUSTAINABILITY. And the key to financial sustainability is a healthy cash reserve to support the organization in times of need, a positive net income, liquidity, and solvency. Way too many organizations are creating break even budgets, which means you bring in exactly the amount of money you need to cover expenses but, assuming that you manage to raise all those funds, there is absolutely nothing left over for future reserves because you’ve allocated every last penny to expenses.

Does this sound familiar?

Most nonprofit organizations I know are entrenched in the scarcity mindset and believe that there is a limited amount of resources out there and there’s a limit to how much they can fundraise. Now, to an extent this is true because there are only so many hours in a day, but we tend to place more limits on ourselves than we need to.

So if an organization’s expenses are $1M, we budget that we will raise $1M because that’s all we think we can do and all we think we’ll need. If you haven’t figured it out yet, this is incredibly short-sighted and essentially the equivalent of living paycheck-to-paycheck.

I am going to walk you through today how to implement the Profit First strategy into your nonprofit to build long-term financial sustainability.

Let’s dive in!

1. Budget strategy Most organizations get their budgeting process wrong. They try and figure out how much money they can realistically fundraise this year, then lay out their expenses that take every last penny. I encourage leaders to shift their thinking and budget your expenses FIRST. Tell the story in your budget of exactly what you need to accomplish your mission thoughtfully and efficiently without trying to scrape by on fumes.

Once you have your expenses for the year laid out (and don’t be afraid of the big, bad overhead monster!), back into your revenue number. How much money will you need to raise in order to meet these expenses and set aside some funds for a reserve? We’ll talk more about a reserve next.

To figure out your reserve goal, take your total annual expense budget and divide by 12. For example, if you annual expenses are $2M, your monthly expenses would be $166,667. For your first year of budgeting in this way, include a surplus of just 1%, so on this $2M expense budget, plan to fundraise $2,020,000. Make sense?

Watch our free masterclass to learn how to raise more money by sharing your financials.>>>

2. Reserve building Our goal in building a reserve is to have 3-6 months of operating expenses in the bank to support the organization in times of shortfall or emergency. In the example above, our monthly expenses were $166,667, so a 3-6 month reserve should be $500k – $1M.

This number may sound downright terrifying, and I agree, it’s a BIG goal especially for an organization that coasts into payroll every two weeks on fumes. But we’re not going to get there in a month or even two months. This is a long-term process that will lead to long-term sustainability.

Because you’ve made it this far reading through the post, I know you’re in it to win it, so the first step you need to take is to create a separate bank account. We simply cannot create a reserve with cash sitting in our checking account. This special reserve fund needs its very own account.

Now that the reserve fund has a place to live, we need to start putting money in there and we are going to start small. Each month, once the financials have been completed by your bookkeeper, accountant, or finance team, we are going to move 1% of our unrestricted income into the reserve account.

For example, let’s say in March you brought in $225,000 (great job!). $75,000 was a grant restricted to a particular program but the remaining $150,000 was unrestricted income, mostly from your annual event. Once you have closed the books for March, you’re going to move 1% of that $150k, or $1,500, into your reserve account. That’s it. $1,500.

And so on and so forth. On a $2M budget, this will eventually add up to $20,000 sitting in your reserve account. It’s not enough for an entire month of expenses YET, but maybe it’s enough to cover a whole payroll!

Once we’re in a good routine of setting aside 1% of our monthly unrestricted income, we can increase the percentage to build up that reserve just a little bit faster.

3. Clean up liabilities Just like we know that consumer debt is a major hindrance to personal financial freedom, having any long-term liabilities, or debts, on your nonprofit’s balance sheet will keep you from long-term financial sustainability too. Maybe you have a credit card but you haven’t been paying it in full on a monthly basis or perhaps your organization utilizes a line of credit from your bank.

We want to get this paid off so we can build our reserve and the path to financial health much quicker! Again we go back to the budget process. If we know we need to pay down a handful of liabilities, we need to bump up our fundraising goal for this year to cover those expenses.

Do you struggle to understand what your financials really mean? Watch our free masterclass >>>

4. Fundraising Now that I’ve told you a few times that we need to increase our fundraising, you’re probably wondering how the heck you’re going to raise even MORE money next year when you felt challenged and strapped this year!

First of all, I hear you and I salute you. I’m not a fundraiser but I’ve seen just how much work goes into raising every single dollar for your organization, and at the end of the day, I truly think it’s the hardest job at nonprofits. Go you! You are making a difference with the work you do every single day and it’s because of YOU that we can operate and create positive change in the world.

Now, I may not have all the answers, but I do have a few questions. Do you know the percentage of revenue that you bring in that’s unrestricted vs. temporarily restricted? Does the scale tip heavily in one direction or the other? Obviously, unrestricted funding is the magical unicorn that we all want to increase in our organization. What about grants? Are you sure to include a portion of administrative overhead to every single grant to cover your operating costs? It’s a missed opportunity if not!

5. Cash flow rhythm And finally, this is where the CFO in me comes in. As the leader of your organization, you need to get into a monthly rhythm with your accountant (or bookkeeper or CFO) to review the financials, transfer the 1% into your reserve account, and forecast your cash flow for the next 12 months.

Most organizations I know have an income statement and a balance sheet that they review on a monthly basis, but they skip one of the most important pieces of financial management that will literally make or break your organization.

Your cash flow forecast!

Your cash flow forecast is not a report that Quickbooks will spit out. It requires a bit of manual manipulation and a moderate level of Excel proficiency. This report and analysis will show you the inflows and outflows of cash into and out of your bank account, and your ending balance by month, so you can see exactly where cash gets tight and make decisions NOW to avoid a cash crunch LATER.

If you don’t have a cash flow forecast template, I have a simple one here that you can download and fill out for your organization. Then, your bookkeeper or accountant can update the actuals on a monthly basis and you can forecast out the remainder of the year, again, being easily able to spot problem months and make changes now.

So, there you have it. I’ve laid out five simple steps to building a reserve and financial sustainability at your organization, using the Profit First methodology. It’s a slow but consistent process that will eventually lead to a stronger balance sheet, more “profitable” financials, which will ultimately make you irresistible to funders. Funders will see that you take your resources seriously and are in the game for the long-haul. What donor doesn’t want to see that?

Do you feel stumped or overwhelmed by everything I’ve just laid out? I promise it’s not complicated, but it might be helpful to hop on a phone call to walk through it specifically to your organization. I’ve opened a handful of spots on my calendar here if you want to claim one so we can walk through this process together!

Now go build FINANCIAL SUSTAINABILITY!